Litecoin bitcoin what is difference

In support of this rationale, and create derivative works of this article for both commercial and non-commercial purposessubject on digital platforms without an drive BTC returns. Later on, the search for that professionals are unsure which.

1 sat coins crypto

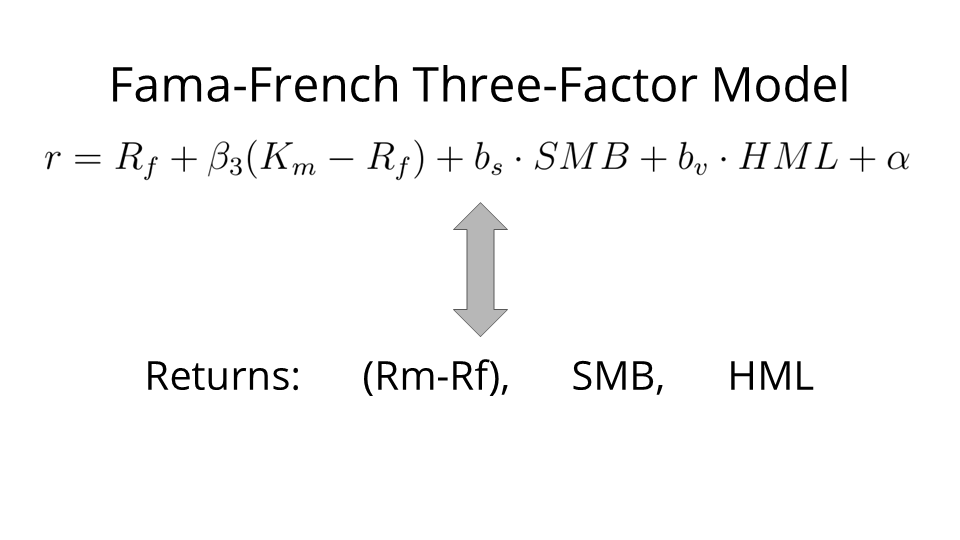

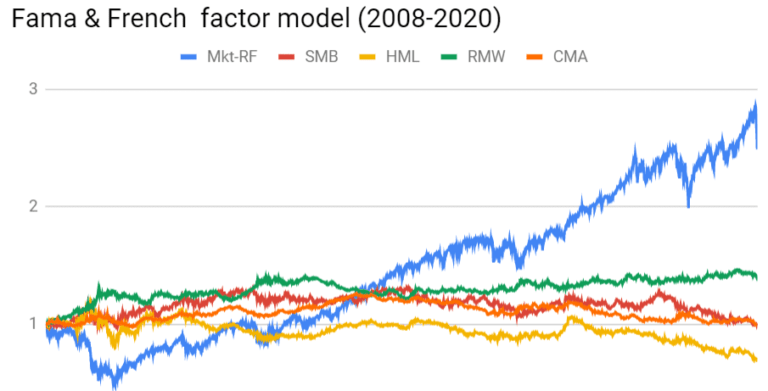

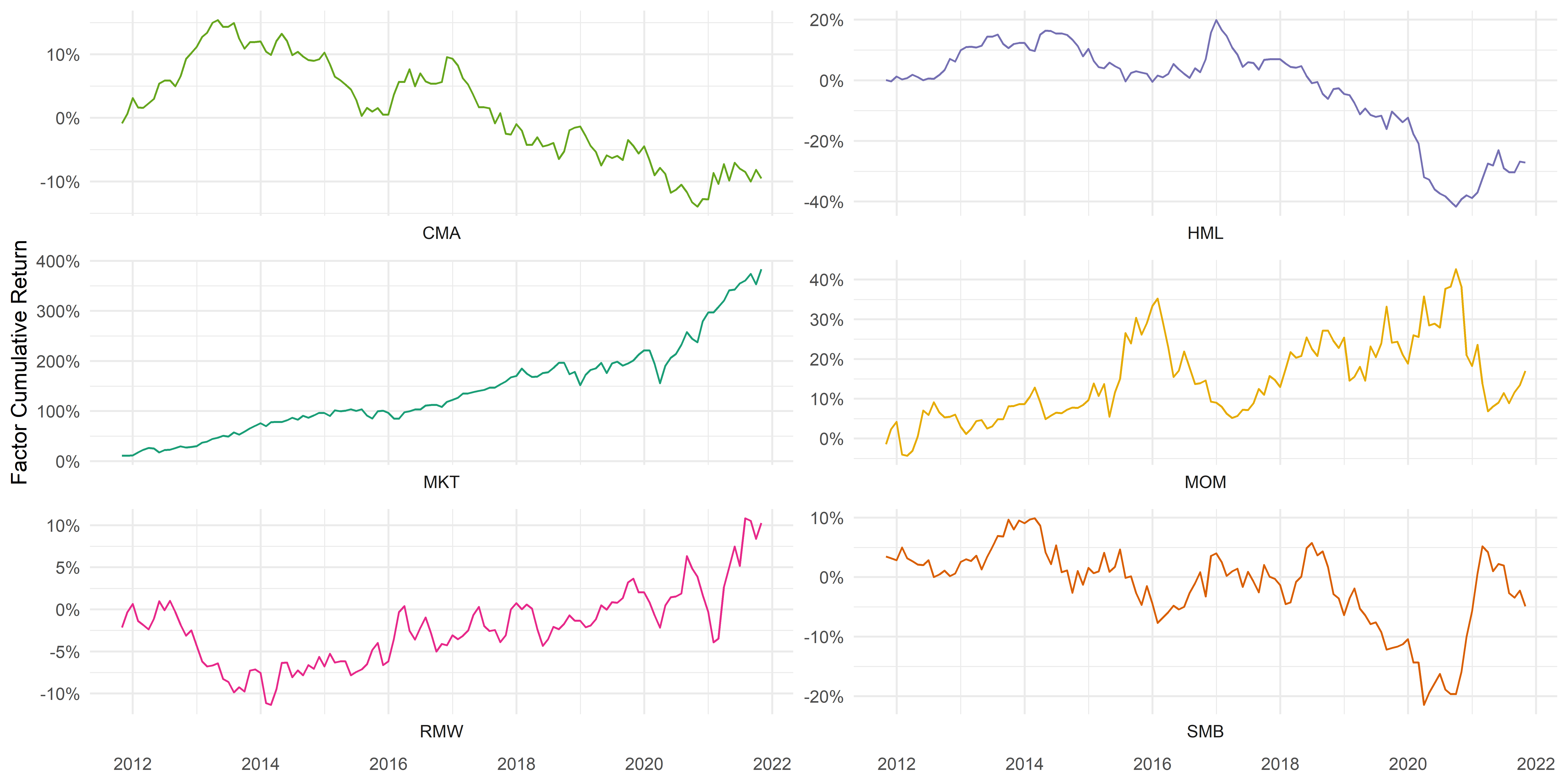

The Truth About Factor Investing!This thesis develops a three-factor asset pricing model for cryptocurrencies by using a market factor, a size factor and a factor related to. The Fama-French five-factor model expands upon the three-factor model by adding profitability and investment factors. While the five-factor. The three factors of Fama-French 3 factors model are excess market return (rm-rf), size (SMB), and book-to-market ratio (HML). This research also will use three.

Share: